When Gatorade launches a 75% lower sugar formula, when Coca-Cola introduces Power Water to compete with PepsiCo’s Propel, and when Nongfu Spring enters the electrolyte beverage category in China, one signal becomes impossible to ignore: Low-sugar electrolyte drinks are rapidly evolving from a niche sports recovery product into a mainstream hydration solution.

When Gatorade launches a 75% lower sugar formula, when Coca-Cola introduces Power Water to compete with PepsiCo’s Propel, and when Nongfu Spring enters the electrolyte beverage category in China, one signal becomes impossible to ignore: Low-sugar electrolyte drinks are rapidly evolving from a niche sports recovery product into a mainstream hydration solution.

Consumers today are no longer satisfied with beverages that simply provide energy or refreshment. They want drinks that support health, hydration, and active lifestyles—without excessive sugar.

As a result, electrolyte drinks are moving beyond their traditional role in sports nutrition and entering everyday scenarios such as:

commuting

office work

travel

outdoor activities

gaming or studying

According to the latest industry data:

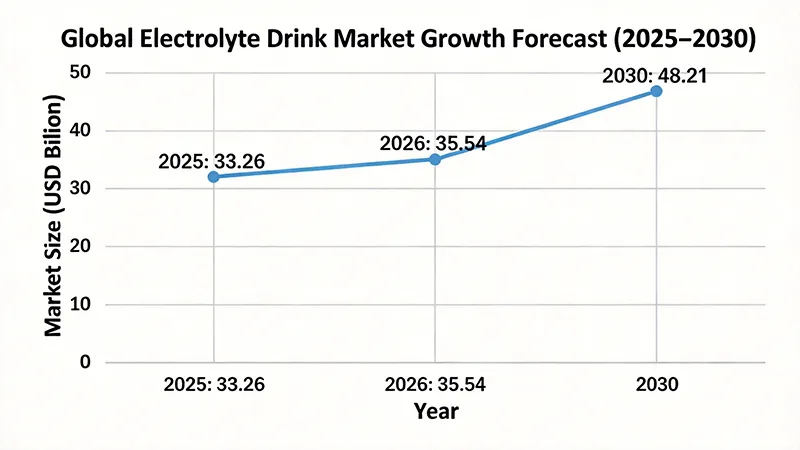

The global electrolyte drink market is expected to reach $35.54 billion in 2026, growing 6.8% year-over-year.

By 2030, the market could surpass $48.21 billion, driven largely by low-sugar and clean-label innovations.

In China, the electrolyte beverage category recorded 32.7% sales growth in 2025, highlighting strong consumer demand.

This article explores the market data, product innovation, and consumer behavior behind this fast-growing category—and what it means for beverage brands planning to launch new functional drinks.

Market Validation: The Numbers Behind the Trend

Global Electrolyte Drinks Market Size & Growth

The global electrolyte beverage market has expanded significantly in recent years.

According to Research and Markets (January 2026), the category shows steady long-term growth:

Year

Market Size

2025

$33.26 Billion

2026

$35.54 Billion (+6.8%)

2030

$48.21 Billion

This represents a compound annual growth rate (CAGR) of 7.9%, making electrolyte beverages one of the fastest-growing segments in the functional beverage industry.

Key Drivers of Growth

Several major forces are driving the rapid growth of low-sugar electrolyte beverages around the world.

Rising Sports Participation

Global participation in sports, fitness training, and recreational activities continues to increase every year.

According to industry surveys, 80% of Americans aged six and above participate in at least one form of physical activity annually, which directly increases the demand for hydration solutions.

As more consumers engage in activities such as running, cycling, gym workouts, and outdoor sports, they require beverages that help restore hydration and electrolytes lost through sweat.

This shift is turning electrolyte drinks into a regular part of active lifestyles rather than an occasional sports supplement.

Everyday Hydration Scenarios

Electrolyte drinks are no longer consumed only after intense exercise.

Electrolyte drinks are increasingly consumed outside traditional sports settings.

Consumers now drink them during office work, travel, outdoor leisure, gaming, studying, and long commuting hours.

Many brands are repositioning electrolyte beverages as “better-for-you water alternatives”, appealing to consumers who want functional hydration without excessive sugar.

This transition from sports recovery to daily hydration dramatically expands the potential market size.

This shift from sports recovery to everyday hydration significantly expands the market potential.

Low-Sugar and Zero-Sugar Demand

Health-conscious consumers are actively reducing sugar intake.

Consumers are becoming more aware of the negative health effects of excessive sugar consumption.

As a result, beverage companies are reformulating products to reduce sugar content while maintaining taste and functionality.

Industry reports indicate that 36% of beverage companies have introduced low-sugar formulas, while many others are investing in natural sweeteners such as stevia and monk fruit.

These changes align with the broader global trend toward healthier functional beverages.

Low-sugar electrolyte drinks are therefore becoming a core product innovation strategy for beverage companies worldwide.

China’s Unique Market Momentum

China represents one of the fastest-growing electrolyte beverage markets.

Recent data shows:

The electrolyte beverage category recorded 32.7% year-over-year sales growth in 2025.

According to Kantar Consumer Index, electrolyte beverages achieved 25% growth within China’s functional beverage segment.

This rapid expansion is driven by several factors:

rising interest in fitness and outdoor activities

hot climate in many regions

increasing awareness of hydration and electrolyte balance

strong distribution networks of major beverage brands

Major Players & Latest Product Launches (2026)

Gatorade Lower Sugar – 75% Less Sugar

In March 2026, Gatorade announced a new sports drink line with 75% less sugar compared to its traditional Thirst Quencher series.

Key product highlights include:

no artificial flavors

no artificial sweeteners

no artificial colors

significantly reduced sugar content

The brand describes the product as:

“science-backed hydration aligned with what today's active consumers are asking for.”

Strategic Meaning

This launch reflects Gatorade’s broader strategy to expand beyond professional athletes and target “everyday movers”—consumers who exercise casually but want healthier hydration options.

Coca-Cola Power Water – Challenging Propel

In October 2025, Coca-Cola launched Power Water through its BodyArmor Sports Nutrition division.

This product marks the first major innovation under the Powerade brand in five years.

Key product features include:

zero sugar formula

electrolyte levels 50% higher than leading electrolyte waters

520 mg sodium and 150 mg potassium per bottle

four flavors including Mountain Berry Blast and Tropical Pineapple

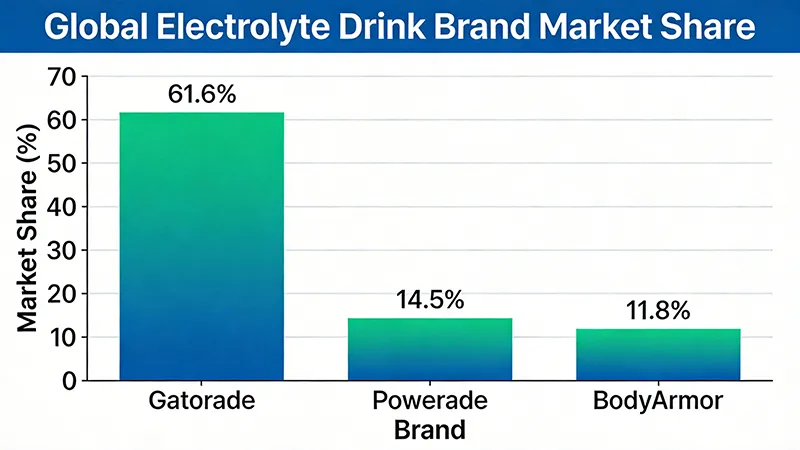

Market share in the electrolyte drink category currently stands at:

Gatorade – 61.6%

Powerade – 14.5%

BodyArmor – 11.8%

Power Water allows Coca-Cola to strengthen its position against PepsiCo’s Propel.

Beyond Immerse – Plant-Based Protein + Hydration

Beyond Meat’s parent company recently launched Beyond Immerse, a hybrid beverage combining hydration and plant-based nutrition.

Product highlights include:

10g or 20g plant protein per can (pea protein)

7g fiber from cassava

zero sugar formula

Flavors include:

Cherry Berry

Strawberry Lemonade

Piña Colada

Cucumber Grapefruit

This product represents a new direction in functional beverages by combining protein, hydration, and fiber.

Cadence Core Hydration – Zero Sugar RTD

UK brand Cadence introduced a ready-to-drink electrolyte beverage with zero sugar and zero calories.

The drink uses steviol glycosides produced through enzymatic processes as a natural sweetener.

Electrolyte composition per 330 ml can:

Sodium – 500 mg

Potassium – 190 mg

Magnesium – 30 mg

The product is suitable for:

vegan diets

ketogenic diets

everyday hydration

Nongfu Spring Enters the Electrolyte Market

In February 2026, Chinese beverage giant Nongfu Spring quietly launched a new electrolyte beverage.

Product highlights include:

low sugar positioning

sugar content: 4.5 g per 100 ml

grapefruit flavor with 500+ mg electrolytes per bottle

lemon flavor with 350+ mg electrolytes

Retail pricing is approximately 3.67 RMB per bottle.

With more than two million retail outlets, Nongfu Spring can rapidly scale distribution and strengthen its functional beverage portfolio.

What “Low-Sugar” Really Means: Formulation Trends

Sugar Reduction Strategies

Different brands use different approaches to reduce sugar while maintaining taste.

Brand

Sugar Level

Sweetener

Positioning

Gatorade Lower Sugar

-75%

Not disclosed

Everyday sports

Cadence

Zero sugar

Steviol glycosides

Daily hydration

Beyond Immerse

Zero sugar

Plant-based formula

Fitness hydration

Nongfu Spring

Low sugar

Not disclosed

Daily hydration

Electrolyte Profiles

Most modern electrolyte drinks focus on a balanced combination of key minerals:

Sodium to enhance water absorption

Potassium to support muscle function

Magnesium for energy metabolism

Calcium for nerve signaling

For example:

Cadence formula per can:

Sodium 500 mg

Potassium 190 mg

Magnesium 30 mg

Power Water formula per bottle:

Sodium 520 mg

Potassium 150 mg

Natural & Clean Label Trends

Consumers increasingly prefer beverages with natural ingredients and transparent labeling.

Industry data shows:

51% of consumers prefer drinks containing natural electrolytes

36% of companies have launched low-sugar beverages

28% expanded mineral-based product lines

Natural electrolyte sources

Natural ingredients are increasingly important in functional beverages.

Many consumers prefer electrolyte drinks derived from natural mineral sources rather than synthetic additives.

Common natural electrolyte sources include:

Sea salt Sea salt is one of the most natural sources of sodium and trace minerals. It is often used in clean-label hydration beverages to provide electrolytes while maintaining a natural ingredient profile.

Coconut water Coconut water is naturally rich in potassium and has been widely marketed as a natural sports drink. It provides mild sweetness and hydration benefits without requiring significant added sugars.

Fruit powders Fruit powders made from citrus fruits, berries, or tropical fruits can deliver natural flavor while contributing small amounts of minerals and vitamins.

Mineral water concentrates Some premium functional beverages use mineral-rich water sources that naturally contain electrolytes such as magnesium and calcium.

These natural ingredients help brands position their products as clean-label functional beverages, which is increasingly important for younger consumers.

Consumer Behavior: Why Low-Sugar Is Winning

The “Better-For-You” Shift in Retail

Retail data from convenience stores shows a clear shift toward healthier beverages.

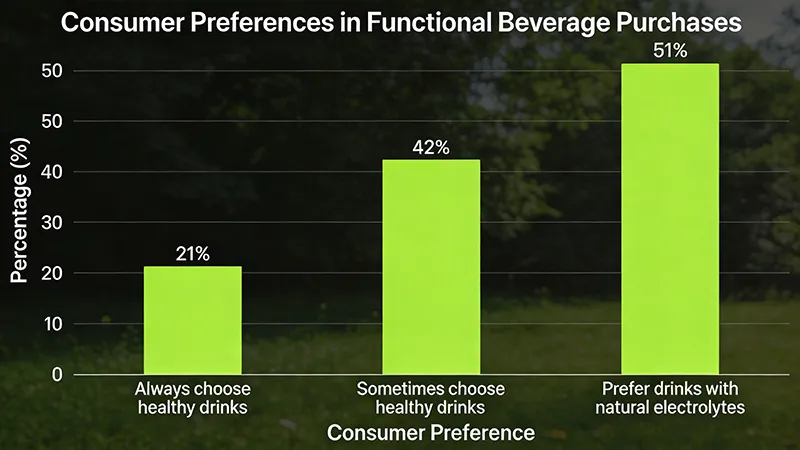

63% of beverage shoppers actively look for healthier options

21% always choose healthier beverages

42% sometimes choose healthier beverages depending on the situation

This indicates that consumers are balancing health goals with convenience and taste.

Key Consumer Segments

Several consumer groups are driving demand for low-sugar electrolyte beverages.

Fitness Enthusiasts

Regular gym users and athletes often lose significant electrolytes during training sessions.

Approximately 58% of fitness enthusiasts report using electrolyte drinks as part of their workout routine.

These consumers prefer beverages that support recovery and hydration without excessive calories.

Millennials

Millennials are highly health-conscious and actively read nutrition labels.

Research shows 49% of millennials prefer vitamin-enhanced water or functional beverages compared with traditional sugary drinks.

They are particularly interested in beverages with natural ingredients and reduced sugar content.

Gen Z and younger consumers

Younger consumers are drawn to beverages that combine flavor, function, and convenience.

Studies indicate 59% of younger consumers prefer flavored vitamin waters, while 52% favor drinks that contain electrolytes.

This group is also strongly influenced by sustainability and clean-label trends.

Natural & Plant-Based Preference

Consumers increasingly favor plant-based and natural products.

Research indicates:

51% of consumers prefer drinks containing natural electrolytes

49% are attracted to clean-label ingredient lists

This trend is driving innovation in plant-based functional beverages.

What This Means for Beverage Brands & Manufacturers

Different regions show different consumption patterns.

North America

largest market

strong demand for low-sugar beverages

Asia-Pacific

fastest-growing region

China market growth above 30%

Europe

strong sustainability standards

high demand for natural ingredients

Future Outlook: Where Is the Category Going?

Projected Growth Through 2030

The electrolyte beverage market is expected to maintain strong momentum.

2026: $35.54 billion

2030: $48.21 billion

The organic sports drink segment is expected to grow even faster with a CAGR of 12.6% from 2025 to 2034.

Key Trends to Watch

Several major trends are expected to shape the electrolyte beverage market over the next decade.

Low-sugar formulas are becoming the industry standard

As consumer awareness of sugar consumption grows, low-sugar formulations will no longer be a niche offering.

Instead, they are likely to become the default expectation for functional beverages, especially in developed markets.

Growth of natural electrolyte ingredients

Brands are increasingly using ingredients such as coconut water, sea salt, and fruit concentrates to create more natural formulations.

These ingredients help companies respond to the growing demand for clean-label and plant-based products.

Sustainable packaging innovation

Packaging sustainability is becoming a major differentiator in the beverage industry.

Materials such as recyclable aluminum cans and rPET bottles are gaining popularity among environmentally conscious consumers.

Hydration scenario segmentation

Functional beverages are increasingly tailored to specific use cases such as:

pre-workout hydration

during-exercise electrolyte replenishment

post-exercise recovery

everyday hydration

This segmentation allows brands to develop multiple product lines targeting different consumer needs.

Conclusion & Action Plan

Low-sugar electrolyte drinks are emerging as one of the most important trends in functional beverages in 2026.

Key takeaways include:

The global electrolyte beverage market is expected to reach $35.5 billion in 2026

Major beverage companies are launching low-sugar products

Electrolyte formulas are evolving toward balanced mineral profiles and clean-label ingredients

Hydration drinks are expanding from sports to everyday consumption scenarios

For beverage brands planning new product launches, several steps are recommended:

Define the product positioning: professional sports or everyday hydration

Choose a sugar strategy: zero sugar, low sugar, or natural sweeteners

Design electrolyte profiles based on scientific ratios

Select packaging that matches brand positioning

Working with an experienced manufacturing partner can significantly accelerate product development and market entry. Integrated beverage OEM manufacturers with strong supply chain capabilities can ensure consistent quality, reliable production, and efficient delivery.

For example, manufacturers with 100% on-time delivery rates and around 80% customer reorder rates demonstrate strong operational reliability—an important factor for beverage brands entering competitive markets.

If you are planning to develop electrolyte drinks or functional beverages, feel free to Contact Us to discuss custom formulation and packaging solutions.

FAQ

What is a low-sugar electrolyte drink?

A low-sugar electrolyte drink is a hydration beverage that contains minerals such as sodium and potassium while reducing sugar content compared to traditional sports drinks.

Are low-sugar electrolyte drinks healthier?

They can be healthier for consumers who want hydration without high calorie intake, especially when combined with natural ingredients and balanced electrolytes.

Why are beverage companies launching low-sugar drinks?

Consumer demand for healthier beverages and lower sugar intake is driving innovation in functional beverage categories.

What packaging is best for electrolyte drinks?

PET bottles are common for mass distribution, while aluminum cans are increasingly used for premium functional beverage brands.

Can beverage brands develop custom electrolyte drinks?

Yes. Beverage OEM manufacturers can support formulation development, packaging design, and large-scale production for private label electrolyte drinks.